Cashback Isn’t a Feature Anymore

Leading platforms are turning cashback into a driver of engagement, retention, and ecosystem growth.

Cashback used to be a simple rebate — predictable, passive, and easy to ignore. Today, it’s being redesigned into something far more strategic. Across Europe and beyond, cashback is evolving into a core engagement layer embedded in digital ecosystems, shaping how users shop, pay, and return to apps. What changed is not the reward itself, but how companies structure it.

At its core, modern cashback systems are built on two key decisions: what triggers the reward and how that reward is delivered. Traditional models still rely on passive triggers, where cashback is automatically credited after a card payment — Apple’s Daily Cash being the most refined example, prioritizing simplicity, transparency, and trust.

More advanced models shift the trigger earlier in the journey. Users activate offers before paying, start purchases within a platform, or encounter rewards directly during browsing. Klarna, for example, turns cashback into part of the shopping flow by rewarding users only when purchases begin inside its app, effectively positioning itself as a gateway to commerce. In these systems, cashback is no longer a post-transaction benefit — it becomes part of the experience itself.

How Cashback Formats Shape Behavior

Cashback is no longer always “cash.” While direct payouts remain the most transparent format, many platforms are reshaping how value is delivered. Rewards are increasingly stored in ecosystem wallets, converted into points or coins, or applied as discounts at checkout. These formats are not just cosmetic variations — they actively influence user behavior.

Apple leans into direct cashback to reinforce simplicity and trust. Klarna stores rewards in its own balance, encouraging users to spend them within the same ecosystem. Polish e-commerce marketplace Allegro converts rewards into coins, introducing accumulation and gamification into the experience. Others, like Monzo, take a different approach by separating cashback into a dedicated “Cashback Pot,” making rewards more visible and increasing their perceived value.

Each format drives a different outcome. Cash builds trust but requires no interaction. Wallet balances encourage reuse. Points and coins create engagement through accumulation. Visible reward containers strengthen ownership. Coupons drive immediate action but are tied to specific conditions.

What looks like a UX decision is often strategic — balancing simplicity, engagement, and retention.

This is also where the gap between traditional banks and newer players becomes visible. Banks largely continue to treat cashback as a feature — often campaign-driven and separated from the core experience. Neobanks, marketplaces, and telecom platforms treat it as a system, combining multiple reward formats and trigger models into integrated environments.

Cashback is Becoming Infrastructure

The result is a shift from one-off rewards to continuous engagement loops. Cashback is no longer a moment tied to a transaction, but a mechanism that encourages users to return, interact, and stay within a platform.

Leading platforms now combine multiple approaches. A single journey can include activating an offer, starting a purchase within the app, earning rewards as points, and redeeming them as a discount — all within one ecosystem. Revolut exemplifies this approach by connecting rewards across payments, travel, and lifestyle services, turning cashback into a unifying layer across multiple user journeys.

Some players are pushing the interaction even further. Banks like the Czech ČSOB embed rewards into conversational interfaces, allowing users to discover and use cashback through an AI assistant rather than navigating static menus. In these models, cashback becomes part of everyday interactions, not just a feature users actively seek out.

As these systems evolve, relevance becomes critical. Some platforms personalize cashback based on behavior, surfacing offers aligned with how users spend. Others, like Apple, deliberately avoid personalization in favor of consistency and privacy. This creates a growing tension between relevance and simplicity — both of which can drive engagement in different ways.

Ultimately, cashback is no longer just a financial incentive layered on top of a product. It is becoming a connective layer within the product itself — linking payments to commerce, rewards to retention, and users to partner ecosystems.

In that sense, cashback is quietly becoming infrastructure — not just rewarding transactions, but shaping how users move through entire ecosystems.

The Latest

#NewProductsandServicesN26 Launches Parent-Controlled Debit Card for Kids

N26 is entering youth banking with a new under-18 debit card for ages 7–17. The product is fully parent-controlled, with accounts managed inside the parent’s app—kids don’t get their own login.

Each child gets a Mastercard in their name (seven designs available), while parents can send money instantly, set limits, and lock or unlock the card. There’s no overdraft, and spending is capped at the available balance. Notably, it’s physical card only—no virtual card.

The account sits as a separate “Space” within the parent’s N26 account and comes with its own IBAN. To sign up, parents must already be N26 customers and verify the child via a birth certificate.

Pricing depends on the plan: Smart and Go users can add up to two children for free, while Metal supports up to five. Standard users can add one child account with a physical card for a one-time €10 fee.

Available across several European markets, including Germany, Austria, and the Netherlands, the product leans heavily into safety—but limits teen autonomy. Even 16–17-year-olds don’t get full account access, despite support for Apple Pay and Google Pay.

Revolut Bundles £400+ in Perks to Win Gen Z

Revolut is doubling down on younger users by turning its Kids & Teens offering (13+) into a lifestyle bundle—adding perks worth over £400 per year at no extra cost.

The package goes beyond banking, combining services across education, wellbeing, mobility, and creativity through partnerships with apps like Headway, Nibble, SleepCycle, Uber Teen, Notion, Chess, and Picsart.

Rather than positioning these as add-ons, Revolut frames them as practical tools—from learning and productivity to independent travel—aimed at helping Gen Z build real-world skills.

The bundle sits on top of existing features like debit cards, parental controls, allowances, and savings, while also offering tangible savings for parents on subscription services.

Strategically, the move pushes Revolut further beyond banking, positioning it as a lifestyle platform for the next generation—and deepening engagement well before users reach adulthood.

#AIRevolut Deploys AI Voice Agents to Transform Customer Support

Revolut is rolling out AI-powered voice agents in partnership with ElevenLabs, aiming to automate large parts of its inbound customer support.

The system handles routine requests—like card issues, transaction queries, and basic account support—while authenticating users and either resolving issues directly or routing them to human agents when needed. It’s designed as a front-line automation layer, not a replacement for human support.

What sets it apart is the quality of interaction. The agents use natural-sounding voices, are multilingual and operate in real time—critical for a global user base.

Under the hood, the system combines speech-to-text, a large language model, and text-to-speech, orchestrated as an event-driven loop that continuously listens, processes, and responds. Revolut is targeting sub-2-second response times, recognizing that even small delays can break the flow in voice interactions.

The key challenge—and differentiator—is dialogue management: deciding when to listen, when to speak, and how to time responses naturally. Done well, it avoids the typical “voice bot” feel of awkward pauses and interruptions.

Early results are notable. Revolut says resolution times are 8x faster, with 99.7% of calls handled successfully by AI agents.

The company is now exploring how to extend voice AI beyond support into broader parts of the customer journey.

#FraudPreventionRevolut Launches ‘Street Mode’ to Counter Coercion Scams

Revolut is introducing Street Mode, a new security feature designed to tackle a rising threat: “transfer mugging”—where victims are forced to authorize payments under pressure.

Unlike traditional fraud, these attacks involve legitimate user authentication, making them harder to detect. With smartphone theft on the rise, stolen devices often give attackers direct access to banking apps—pushing fintechs to rethink real-world security.

Street Mode adds a location-aware layer of protection. Users define trusted places like home or work, where transactions above a set limit can proceed normally with biometrics.

Outside these zones, stricter rules apply: high-value transfers are delayed by one hour, followed by a second selfie verification before completion.

The delay is key—it creates a window for users to react if a device is stolen or if they’re being coerced.

The feature builds on Revolut’s existing Wealth Protection system, extending it with context-aware controls that adapt to real-world risk—marking a shift from static security to situational fraud prevention.

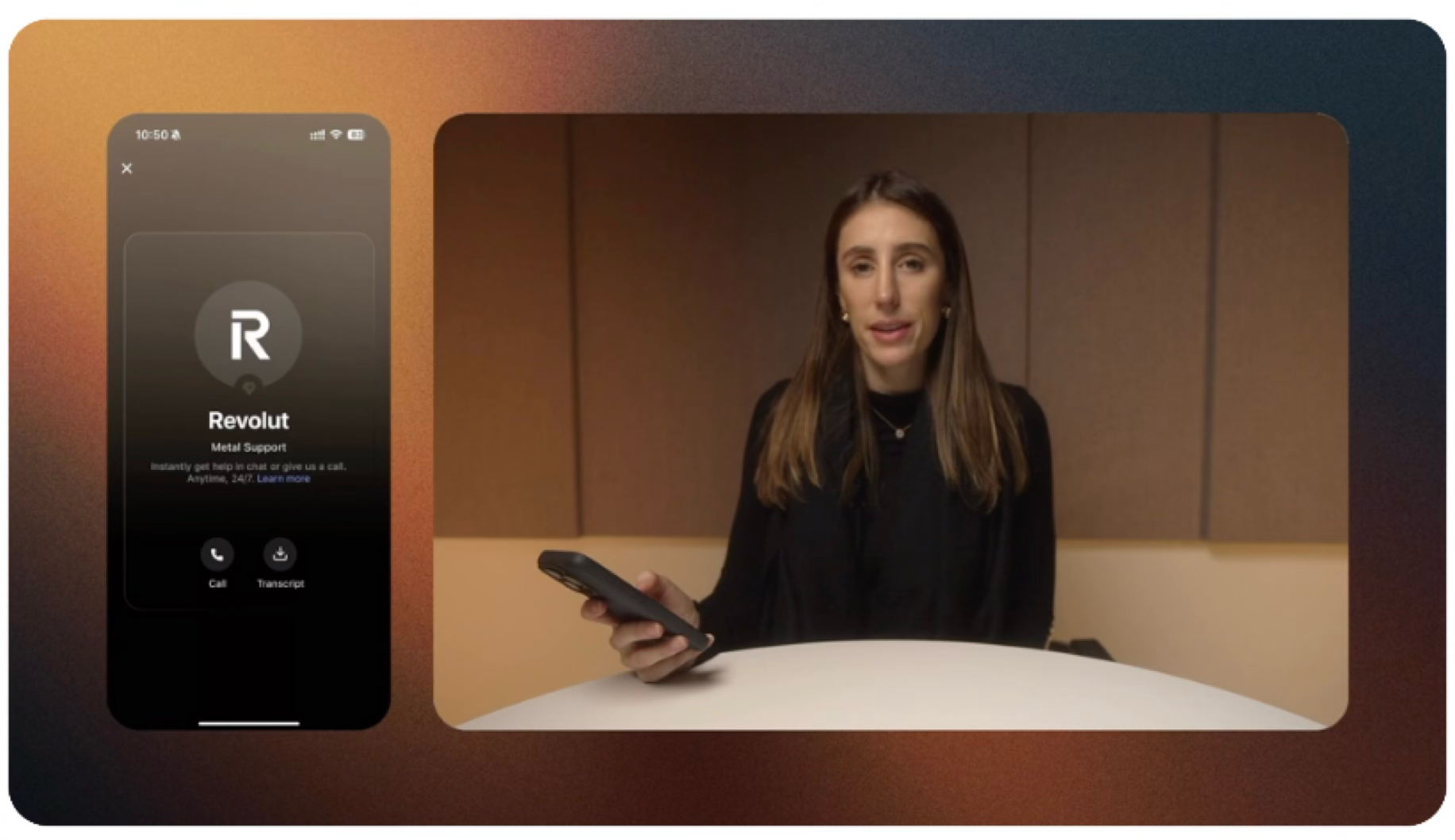

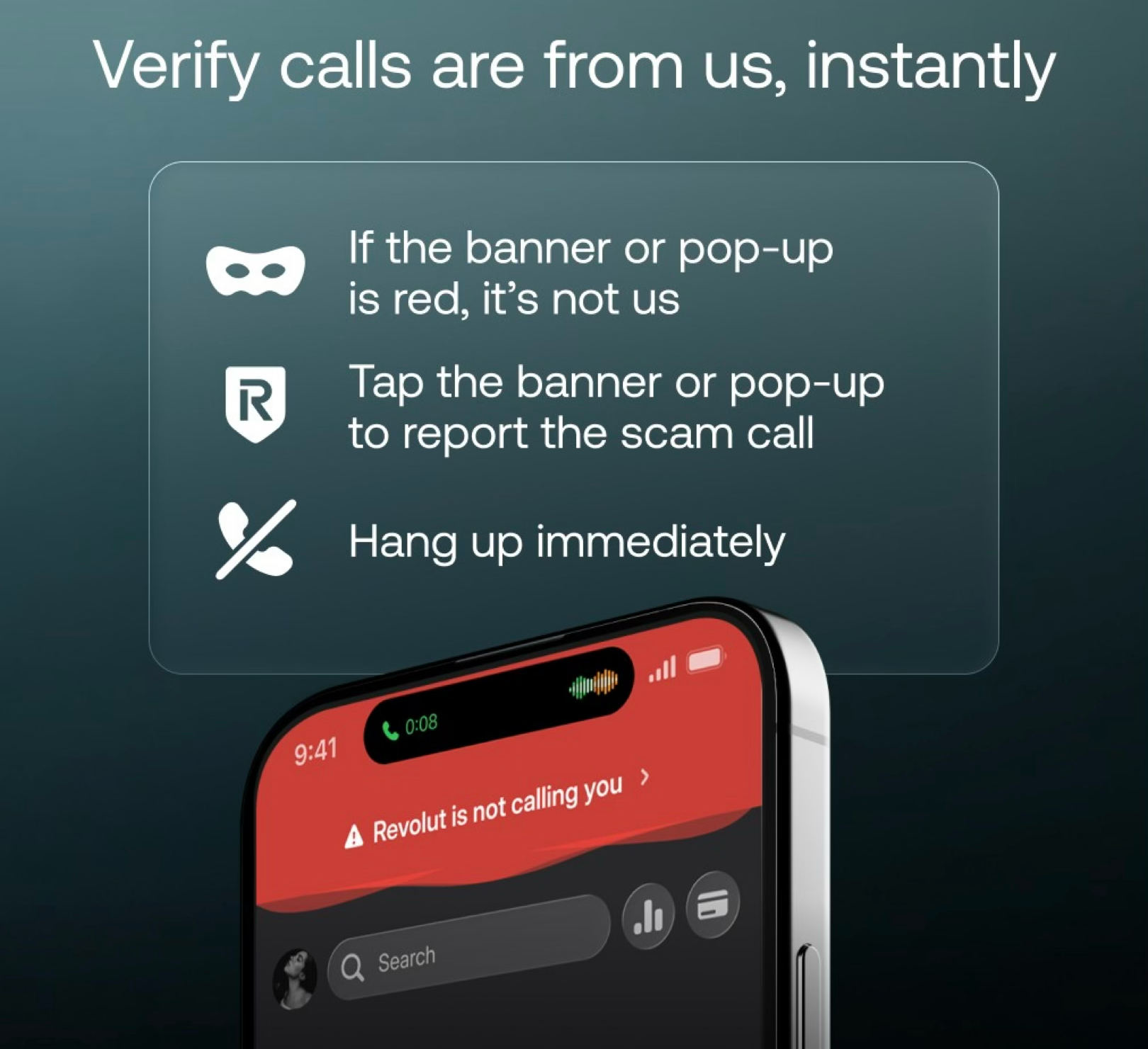

Revolut Adds Real-Time Call Verification to Fight Scams

Revolut is rolling out a new Call Identification feature aimed at tackling the rise of impersonation scams—particularly those powered by AI-generated deepfake voices.

The feature works in real time by detecting when a user is on a phone call, including via third-party voice apps, and verifying whether the caller is actually a Revolut agent. If not, users see a prominent in-app warning banner with guidance on how to report the suspected fraud.

The move targets a growing attack vector where scammers pose as bank representatives to gain access to accounts, increasingly using convincing synthetic voices.

There’s no setup required for most users. The feature is enabled by default on iOS, while Android users can switch it on via Revolut’s Security Hub.

With scams becoming more sophisticated, Revolut is leaning into proactive, real-time protection—bringing fraud detection directly into the moment it matters most.

#WealthBitpanda Becomes a Full Neobroker with Stock Trading Launch

Bitpanda is expanding beyond crypto, launching regulated trading for real stocks, ETFs, and ETCs—marking its shift into full neobroker territory.

The move adds around 10,000 traditional securities to the platform, a major step up from its previous “Bitpanda Stocks” offering, which only provided derivative-based exposure without actual ownership or shareholder rights.

Now, users can buy and own real assets under a regulated custody framework, bringing Bitpanda closer to traditional brokerage models.

Pricing is straightforward: €1 per trade, with fractional investing starting from €1. The platform also handles taxes automatically for users in Germany and Austria.

The shift puts Bitpanda in direct competition with players like Trade Republic and Scalable Capital, while reflecting a broader trend: crypto platforms are increasingly moving into traditional finance to capture a larger share of user wallets.

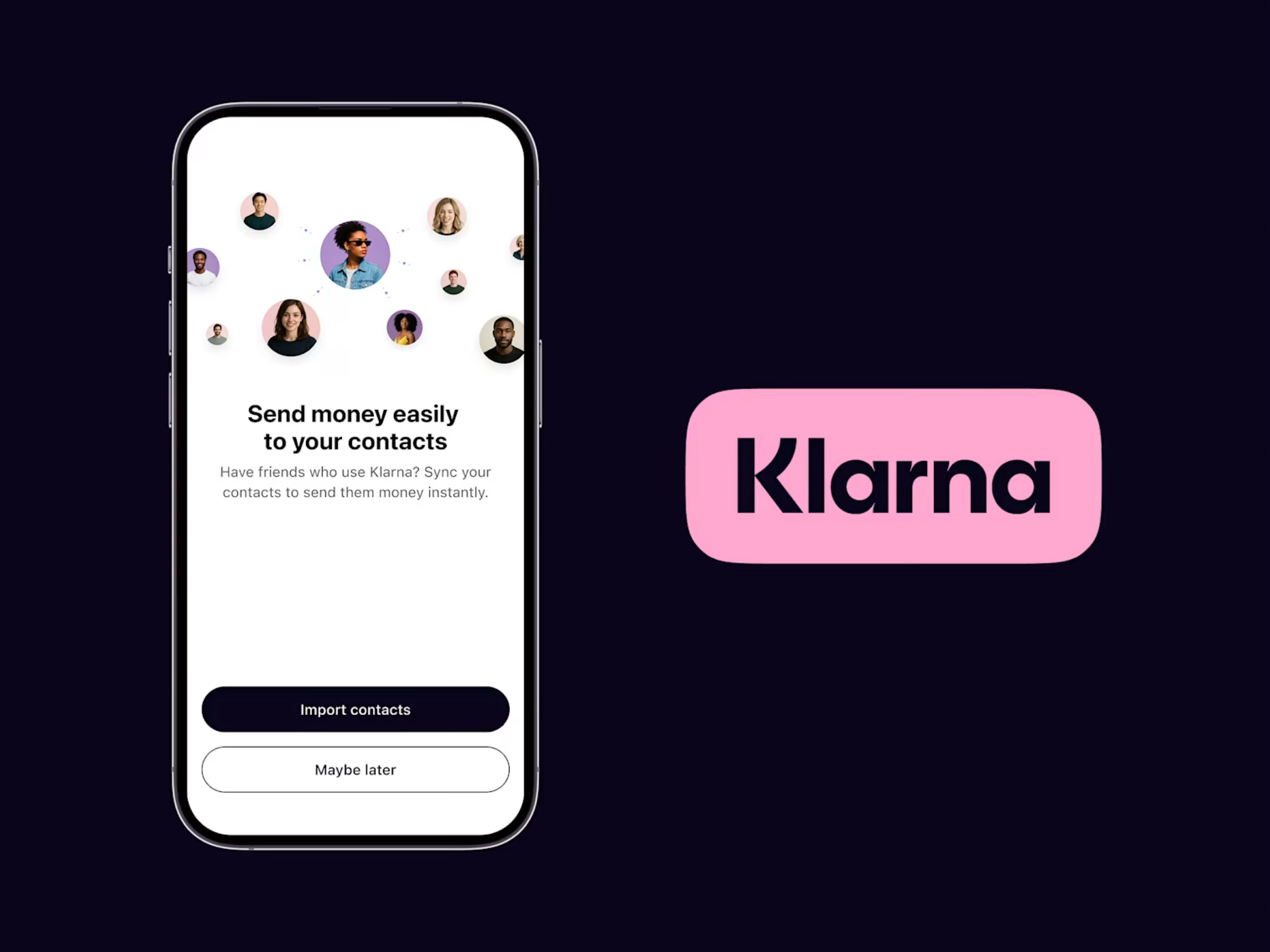

#PaymentsKlarna Adds Instant P2P Payments to Take On PayPal and Wero

Klarna is expanding beyond e-commerce with the launch of instant peer-to-peer payments, allowing users to send money directly within the app.

Transfers can be initiated via phone number, email, QR code, or contacts, with Klarna running fraud and eligibility checks before funds are released. For now, payments are limited to Klarna users, but support for non-users and cross-border transfers is on the roadmap.

The feature is rolling out across 13 European markets, including Germany, the UK, France, Italy, Poland, and Spain.

Longer term, Klarna is exploring blockchain and stablecoin infrastructure to improve speed, scalability, and cost—particularly for cross-border payments.

The timing is notable. P2P payments are already standard for players like PayPal and are becoming a key battleground in Europe with the rise of Wero.

For Klarna, this is part of a broader shift toward becoming a full financial platform. Since launching Klarna Balance in 2024, deposits have grown from $9.5B to $14B, while the Klarna Card has added around 4 million users, now accounting for 15% of total transaction volume.

Wero Scales Up as Europe’s Card Alternative Gains Traction

Wero, the account-to-account (A2A) payment scheme backed by the European Payments Initiative (EPI), is rapidly moving from early rollout to a scaled pan-European network.

Designed as a European alternative to Visa, Mastercard, and PayPal, Wero enables users to send and receive money via phone number or QR code, directly from their bank app or a dedicated wallet—bypassing traditional card rails.

After launching initial services, Wero now supports instant P2P and online payments with immediate settlement, and has already reached 47 million users across key markets including France, Germany, and Belgium. The network is backed by 14 major European banks and two leading acquirers.

Momentum is building across the ecosystem. Revolut joined EPI in mid-2025 and is rolling out Wero payments inside its app in France, Belgium, and Germany. N26 followed with a formal membership, planning to integrate Wero P2P payments starting in H2 2026. On the acquiring side, Raiffeisen Bank International is enabling merchants to accept Wero, while Payment Services Austria is preparing the infrastructure to connect banks across Austria and Germany.

The roadmap goes beyond P2P. In 2026, Wero is expected to expand into in-store payments, subscriptions, BNPL, digital identity, and interoperability across payment systems.

For Europe, Wero is no longer just a strategic ambition—it’s becoming a real contender in reshaping the region’s payment stack.

Europe Links Local Payment Giants Into One Network

Europe is pushing ahead with plans to connect its domestic payment champions into a single interoperable network, aiming to reduce fragmentation across the region.

Wero, the European Payments Initiative (EPI)’s A2A scheme, is teaming up with major local players including Bancomat (Italy), Bizum (Spain), SIBS (Portugal), and Vipps MobilePay (Scandinavia).

At the core is the “Co-Hub”, a technical bridge designed to connect national payment systems without replacing them. Each scheme keeps its brand and user experience, while enabling cross-border interoperability.

The ambition is scale: 100+ million users across 12 countries at launch. In practice, this could allow users to pay across borders seamlessly—like using Wero in Spain even if Bizum is the local scheme.

Rollout is phased, with cross-border mobile payments expected in 2026, followed by e-commerce and POS payments in 2027—marking a major step toward a unified European payments layer.

Pilot Shows Cross-Border Mobile Payments Are Technically Ready

A new pilot suggests Europe’s fragmented mobile payment systems may soon work seamlessly across borders.

In a proof of concept, Poland’s BLIK and Spain’s Bizum successfully completed a real-time cross-border euro transfer, using a phone-number-based routing system linked to SEPA Instant infrastructure.

The setup relies on a mapping mechanism that connects a recipient’s phone number to a euro-denominated bank account, enabling instant transfers without needing card networks.

The pilot is part of the broader EuroPA initiative, which aims to interconnect national payment schemes like BLIK, Bizum, MB WAY, Bancomat, and Vipps.

While still early-stage—with limited participants and no finalized commercial model—the test confirms that real-time cross-border A2A payments in Europe are technically feasible.

What remains open is execution: scaling the model, aligning user experience, and defining pricing across markets.

Thanks for stopping by Beyond George!

Subscribe for free and keep the good stuff coming.