The Rising Star of Eastern Europe

🇵🇱 A Glimpse into Poland's Dynamic Financial Landscape

Since joining the European Union in 2004, Poland’s GDP has grown steadily. Furthermore, it was the only EU country that did not experience a recession in 2009.

Poland is the sixth largest economy in the European Union and its financial services market is the biggest in the CEE region.

According to the European Central Bank value of assets in the Polish banking industry totaled EUR 564 billion in 2021. That’s almost double the EUR 336 billion in the Czech Republic.

The Polish banking landscape comprises 30 commercial banks, 503 local cooperative banks, and 22 cooperative savings and credit unions (SKOK), collectively driving financial services and fostering economic growth.

PKO Bank Polski ranks as the undisputed leader of the Polish banking sector with assets totaling PLN 431 billion. The company serves 11.7 million customers, from which 7.2 million people actively use the IKO application

With over 6.3 million customers, Bank Pekao has the second-largest branch network in the country. As the leading corporate bank in Poland, Bank Pekao counts many of the largest Polish corporations among its clients. The PeoPay application has 2.25 million users who can access accounts and cards, withdraw cash with "Blik," and even take out loans. PeoPay recently added the option to buy public transport tickets and pay parking fees.

A subsidiary of the Santander Group, Santander Bank Polska is a prominent player in the Polish banking market. With a diverse range of financial solutions catering to individuals, businesses, and institutions, Santander Bank Polska serves a total of 5.7 million customers, including 3.4 million digital customers.

ING Bank Śląski provides traditional banking services along with digital solutions for its 4.42 million retail and 543 thousand corporate clients.

With 3.4 million monthly active users of mBank’s mobile application, mBank is known for its digital-first approach and user-friendly banking solutions, serving 4.6 million retail clients and 33 thousand corporate clients in Poland.

Among the other noteworthy banks in Poland, Alior Bank, a leading fintech-focused bank, has gained recognition with 4 million retail customers, including 1 million with Alior Mobile, as well as with their latest BNPL solution, Alior Pay.

When it comes to challenger banks, Revolut stands out as the most prominent on the Polish market, with 2.5 million customers in Poland as of June 2023, and the country has been listed among Revolut's five fastest-growing markets globally.

Over the past 4 years, the number of FinTechs in Poland has nearly doubled - to 299 in 2022.

There are several factors driving this surge, including overall macroeconomic growth, increasing demand for technology-enabled financial services, and changing customer behavior accelerated by the COVID-19 pandemic.

By being the largest financial services market in Central and Eastern Europe, Poland has the potential to attract talent and investment from the entire region.

Polish consumers display openness to innovation and demonstrate a high level of maturity when utilizing digital solutions.

The Polish FinTech Map, developed by Cashless.pl, showcases 15 main fintech segments, with payments, financial management, and software providers emerging as the largest groups, collectively representing nearly 50% of all fintech providers. In addition, segments like InsurTech and Crowdfunding have been identified as "high growth" areas, witnessing dynamic increases in the total number of companies during 2022.

🇵🇱 #SUCCESSSTORIES

🚀 BLIK

BLIK, the revolutionary mobile payment system in Poland, transformed the mobile banking market when it launched in 2015 through a collaboration among six competing Polish banks. Utilizing a user-generated six-digit code in the banking app, BLIK enables e-commerce transactions, ATM withdrawals, POS terminal payments, and peer-to-peer transfers. Its widespread success can be attributed to its convenience, leading to its integration within existing mobile banking apps and establishing itself as the market standard. With a two-minute expiration time for the code, BLIK offers versatility, excellent user experience, and simplicity, garnering praise from its users for its speed, convenience, and security. Currently, BLIK boasts 25.9 million users of mobile bank apps in Poland, with around 12.9 million using it for monthly payments. Expanding beyond Poland, BLIK acquired VIAMO, a mobile payment platform in Slovakia, solidifying its presence in global markets. With aspirations to become a pan-European payment system, BLIK has set its sights on a promising future.

🚀 ALLEGRO PAY

Allegro, one of Poland's largest online shopping platforms and the largest e-commerce player in Europe acquired Mall Group in April 2022, expanding its reach to e-commerce websites in the Czech Republic, Slovakia, Hungary, and Croatia. With Allegro Pay, a new payment method on the platform, users can conveniently defer payments or split them into installments for one or multiple items. The user-friendly service welcomed its first million clients within just 9 months of its launch, offering fast onboarding, one-click payments, and tailored financing plans. Through a simple application process, users gain access to a budget that can be freely used for purchases, providing greater flexibility compared to traditional consumer credit options.

🚀 KONTOMATIK

Kontomatik, a rapidly growing fintech based in Poland since 2009, specializes in financial data aggregation services and offers additional analytical tools. Using Machine Learning, Kontomatik's analytical solutions assess financial data, assign labels to transactions, and provide risk analysis solutions such as scoring for creditworthiness evaluation. With authorization to operate in 17 countries, Kontomatik is recognized as a leading open banking provider in the CEE region. Having served over 200 reputable international clients, including Revolut, Grover, Experian, and Raiffeisen Digital Bank, Kontomatik continues to make its mark in the industry.

The Latest:

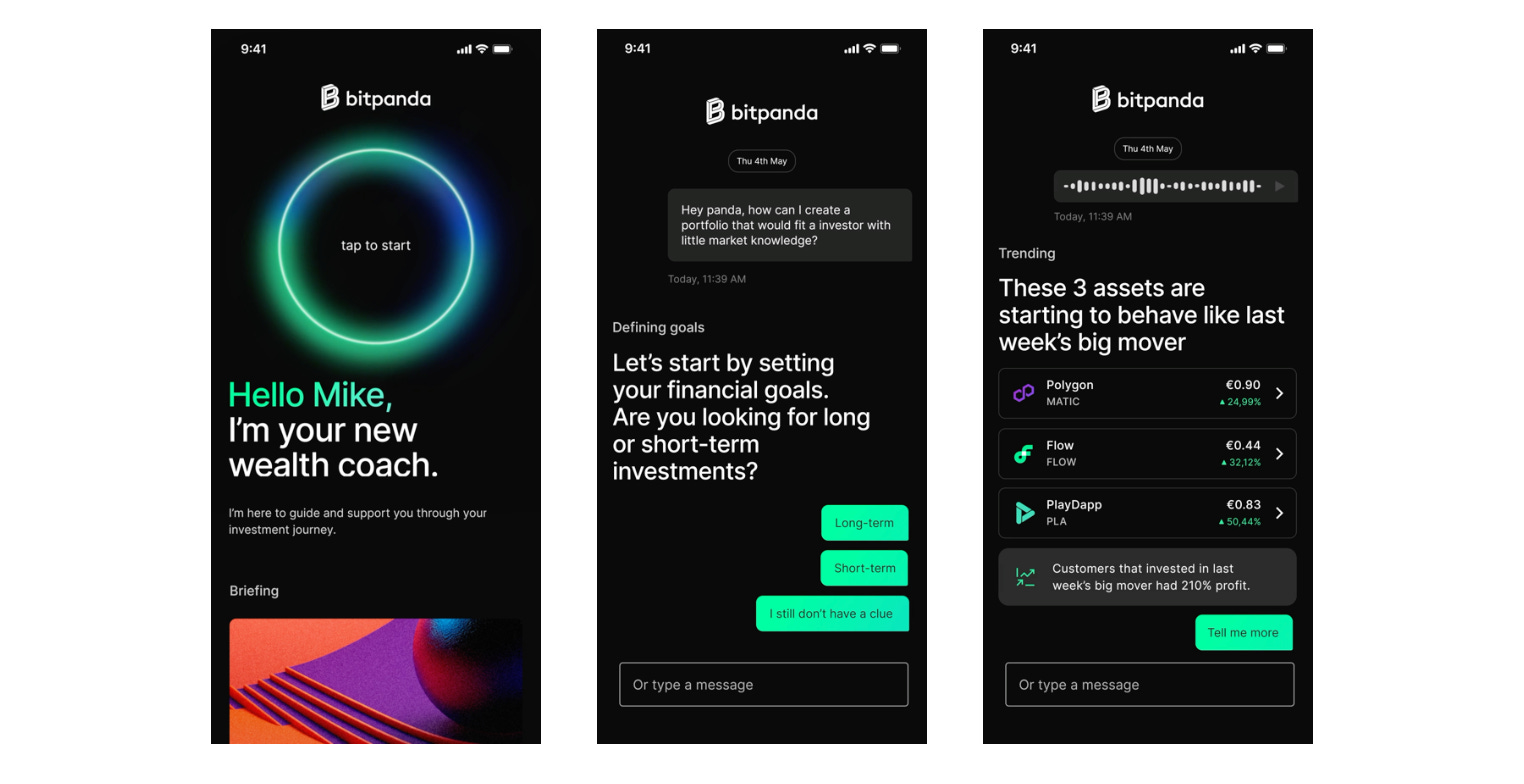

📍Bitpanda.AI

Bitpanda makes a move towards further simplifying investing with the creation of Bitpanda.ai, a dedicated AI division within the company. Among the first products to be rolled out will be a fully conversational AI application that will function as a personalized wealth manager that learns and adapts to the user's needs and makes investing easier and more accessible for new customers. Future releases should include personalized investment products, automated portfolio strategies, and real-time market analysis, however, there is no clear timeline for the launch of Bitpanda's AI advisor. 🔗 Bitpanda Press Release

📍Raiffeisen x Bitpanda 🇦🇹

The Austrian Raiffeisenlandesbank NÖ-Wien together with Bitpanda signed a letter of intent on an exploration of a potential partnership, which would result in including cryptocurrencies and other asset classes into the digital investment offering of Raiffeisen NÖ-Wien with the help of Bitpanda’s infrastructure. Users should be able to invest from as little as 1 euro. Crypto investment should be featured alongside digital investment services for stocks, exchange-traded funds, precious metals, and commodities. The assessment of a potential partnership will continue until the end of this year. 🔗 Bitpanda Press Release

📍Bitpanda x Coinbase

The crypto exchange Coinbase signed a licensing agreement with Bitpanda Technology Solutions based on which Coinbase’s institutional clients can now offer a fully regulated digital asset trading and custody offering globally through one of the most highly regulated partners in the industry. Bitpanda’s infrastructure for flexible and scalable 24/7 trading can be integrated in just 3 months. 🔗 Bitpanda Press Release

📍Revolut Loans

Revolut started offering consumer loans in France after launching in Poland, Lithuania, Ireland, Romania, and Spain. The loan program ranges from € 1,000 to € 50,000, with mortgage loans in future development plans. Revolut has around 30 million customers worldwide, including nearly 2.5 million in France. 🔗 Read more about Revolut Loans

📍ABN AMRO x Gimi

In collaboration with Swedish company Gimi, ABN AMRO has introduced a specialized financial literacy app for children aged 8 to 13. This app allows kids to track their bank balance, communicate with their parents regarding chores and income-generating tasks, and engage in educational quizzes and games to earn points, badges, and diplomas. The app aims to help children grasp the value of money and comprehend proportional amounts.

Originally launched as a pilot project in the Netherlands with 3,000 participants, Gimi proved to be immensely successful. Consequently, the app is now being made available to the general public, regardless of their affiliation with ABN AMRO. The pilot program revealed that children check their account balances an average of five times per week, fostering awareness of their finances and instilling a sense of responsibility.

ABN AMRO has set an ambitious goal of reaching one-third of its 8-13 age group clients over the next three years. With a long-term vision, the bank aims to equip these children with the necessary skills to avoid financial difficulties as they grow older. 🔗 Check out Gimi at ABN AMRO

📍MyMonii

Danish pocket money app MyMonii is now available in Germany for children from the age of 7. The app is designed to help families manage their children's pocket money and comes with an optional VISA prepaid card. The app provides an easy overview of savings and expenses for both parents and their children. Optionally, savings goals and monetary incentives for completing household tasks can be set. The VISA card can be used abroad and online and includes a merchant block on shops that are not suitable for young people. MyMonii’s “Investing” learning tool is currently available only in Denmark. 🔗 MyMonii website

📍Robinhood Europe BV

The Robinhood Wallet has officially been rolled out to more than 1 million iOS users on the waitlist globally. Robinhood Wallet is a multi-chain, self-custody, Web3 wallet that allows users to own and swap crypto, and connect to a wide range of decentralized applications (dapps). The app is the first application of the company available in Germany. Robinhood has already tried entering Europe before, by building a team in London and starting a subsidiary in the Netherlands. At the beginning of 2020, it also explored the investment behavior of German users. Now a new Dutch company named ‘Robinhood Europe BV’ surfaced indicating Robinhood resumed its activity in the European market.

📍Starling ‘Split payment’

Starling Bank customers can now organize their salary payments across their accounts. The new feature, called ‘Split payment’, allows customers “to decide how much of an inbound payment, such as their salary, to put away and where, including their saving Spaces, joint accounts, additional accounts, and Kite cards.” ‘Split payment’ users can organize inbound payments either by value or percentage. With this feature, the bank wants “to give people more control over their budget. The feature is available for Starling’s GBP Current Account and Business Current Account holders. 🔗 Media article on AltFi

📍Raiffeisen Infinity 🇦🇹

Raiffeisenlandesbank Oberösterreich together with Raiffeisenlandesbank NÖ-Wien as lead banks took on the task of developing a new digital solution for corporate customers. Together with Raiffeisen Software GmbH and Netural they have driven the development of Raiffeisen INFINITY for the entire Raiffeisen banking group.

Raiffeisen INFINITY sets new standards for Business banking with features like a simplified login process with an email address, password, and smsTAN or cardTAN, data import via drag & drop, notification center, multi-banking functionality, bank guarantee request process, eSafe or digital estate management. Raiffeisen claimed to receive outstanding feedback and win more and more customers who have been working with ELBA-business for years for the new better solution. 🔗 Link to Raiffeisen INFINITY website

📍NiCKEL

With continuing its growth in Europe, the French payment institution NiCKEL, part of the major European bank BNP Paribas, is entering the German market. NiCKEL's focus is on an easy-to-use, transparent, and accessible financial service for all.

By cooperation with ilo-profit GmbH as a sales partner in Germany, NiCKEL’s services are accessible via a large network of lottery acceptance points. Customers can open an account directly at the kiosk and receive a debit card and a German IBAN, all connected to a digital app. After being present in France, Spain, Portugal, Belgium, and now Germany, the company plans to open branches in seven European countries by 2024. 🔗 NiCKEL website

📍Deutsche Bank & Crypto

Germany’s largest banking institution, Deutsche Bank, has applied for a digital asset custody license to the country’s financial regulator, BaFin.

While Deutsche Bank has been critical of Bitcoin and the crypto market’s volatility over the past few years, its tone toward the industry has changed in 2023.

German securities processor Deutsche WertpapierService Bank, the bank’s investment arm, created a Bitcoin-focused platform, wpNex, for retail customers recently. In February, Deutsche Bank Singapore, successfully completed trials for a tokenized investment platform called Project DAMA (Digital Assets Management Access). 🔗 Link to media article on Coindesk

📍Revolut Ultra

By launching ‘Ultra’ Revolut claims to have released the ultimate traveling and lifestyle companion. The platinum membership plan comes with a Mastercard-branded platinum card and an annual UK fee of £540. The platinum card benefits include subscriptions with various partners like Financial Times or NordVPN, unlimited fee-free international money transfers, 1.2% cashback on Revolut Pro, purchase and refund protection, canceled event protection, unlimited access to 1,400+ airport lounges worldwide, worldwide emergency medical and dental cover insurance, including winter sports and 10% cashback with Revolut Stays. 🔗 Revolut Ultra website

📍Caixa App to POS

CaixaBank has announced a new app that enables contactless payments from Android devices in Spain, becoming the first Spanish bank to enable the service without the need for an additional device.

The Smartphone TPV app will offer functionalities similar to a traditional point of sale (POS) terminal and the option to send the receipt to customers by email or QR code.

The app will be available to businesses, professionals and self-employed of any size and sector, enabling them to accept credit card payments of any amount from mobile devices. 🔗 Caixa bank Smartphone TPV

Beyond George Suggests

📚 Banks and Gen Z /report by TearSheet 👓 Read here

🗞️ Fintech Future’s Banking Technology Magazine /June 2023 issue 👓 Read here

🗞️ INSIGHTS The Financial Brand magazine /Summer 2023 issue 👓 Read here

🎤 SIFTED SUMMIT /4-5 October 2023, London 👉🏻 Conference page

🎤 FINTECH LIVE /8-9 November 2023, London & online 👉🏻 Conference page

🎤 Financial Times GLOBAL BANKING SUMMIT /27-29 November 2023, London & online 👉🏻 Conference page

Last but not least:

Read also our online magazine Fintech & Banking Innovation on Flipboard. Click the Flipboard logo below for access 👇🏻